IFRS 18 Explained: The Biggest Change to Financial Statements Since IAS 1

If you work in accounting, financial reporting or auditing, you’ve probably heard people mention IFRS 18. Many assume it’s “just another accounting standard” but it actually isn’t.

IFRS 18 is the biggest change to the presentation of financial statements in more than twenty years. Although it doesn’t change how transactions are measured, it changes how companies present and explain their financial performance, making financial statements more comparable and transparent.

The standard becomes mandatory for annual reporting periods beginning on or after 1 January 2027, replacing IAS 1. Because IFRS 18 is applied retrospectively, companies reporting under IFRS should already be preparing during 2026.

Why was IFRS 18 introduced?

Investors often complained that comparing companies was unnecessarily difficult.

One company would present “Operating Profit.”

Another would present “Adjusted Operating Profit.”

A third would report several versions of EBITDA without clearly explaining how they were calculated.

Even companies operating in the same industry could produce income statements that looked completely different.

IFRS 18 aims to solve this problem by introducing a more consistent structure for the Statement of Profit or Loss.

What changes?

1. A mandatory Operating Profit subtotal

For the first time, IFRS defines an operating profit subtotal that every company must present.

This should significantly improve comparability between companies.

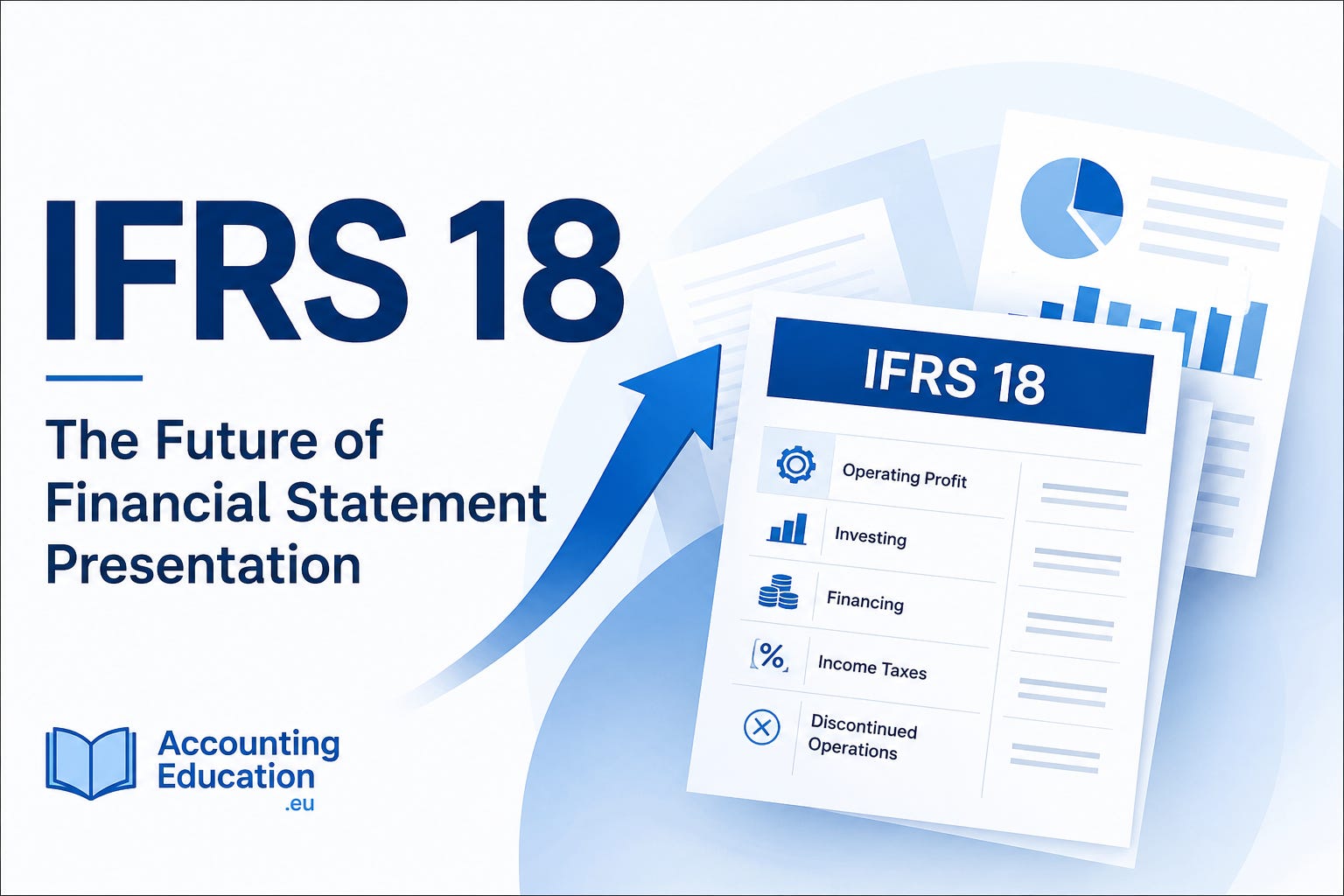

2. New categories for income and expenses

Items in the Statement of Profit or Loss must be classified into specific categories, including:

Operating

Investing

Financing

Income Taxes

Discontinued Operations

This creates a more consistent presentation across industries.

3. Greater transparency around management KPIs

Many companies publish measures such as:

Adjusted EBITDA

Underlying Profit

Normalised Earnings

Under IFRS 18 these Management-defined Performance Measures (MPMs) don’t disappear.

Instead, companies must explain:

how the measure is calculated;

why management uses it; and

how it reconciles to IFRS numbers.

This gives investors much better insight into the figures presented outside the financial statements.

Does IFRS 18 change accounting entries?

No.

This is probably the biggest misconception.

IFRS 18 does not change:

revenue recognition;

depreciation;

inventory accounting;

lease accounting;

impairment calculations.

Instead, it changes how information is presented and disclosed.

The accounting stays largely the same.

The financial statements look different.

Why should accountants care today?

Although the mandatory application date is 2027, comparative information must also be presented under the new format.

That means companies should already be reviewing:

chart of accounts;

reporting structures;

management reports;

ERP systems;

consolidation processes; and

financial statement templates.

Waiting until 2027 will almost certainly be too late for many organisations.

Final thoughts

IFRS 18 isn’t about changing accounting principles.

It’s about making financial statements easier to understand.

For accountants, auditors and finance professionals, the challenge won’t be learning new journal entries—it will be adapting reporting processes, systems and disclosures.

The sooner organisations begin preparing, the smoother the transition will be.

After all, great financial reporting isn’t just about producing the correct numbers—it’s about presenting them in a way that everyone can understand.